Recently a federal court in Northern California found that a document which one party claimed was a non-binding proposal was really a binding ground lease agreement with purchase options, which resulted in a 16 million dollar damage award. The proposal concerned development of the Santana Row project in San Jose. Generally, creating of a valid contract requires mutual assent. An “agreement to agree, ” without more, does not create a contract. In this case the court found more.

In First National v. Federal Realty, First National controlled the property but did not want to sell it yet. Federal unsuccessfully offered to buy, and the parties entered negotiations for a ground lease that lasted several years. They exchanged several proposals, including a “counter proposal” and a “revised proposal.” Finally the both signed a document titled “Final Proposal,” a one page document. Earlier proposals stated that they were non-binding; the final did not include this language. It stated that it was “accepted by the parties subject only to approval of the terms and conditions of a formal agreement,” and Federal was to prepare a formal legal agreement. And it provided that First National could require Federal to buy the property any time over a period of ten years; and that Federal could force First National to sell at the end of ten years (the “Put and Call”). Federal never prepared a formal agreement, and decided it did not want the lease.

In First National v. Federal Realty, First National controlled the property but did not want to sell it yet. Federal unsuccessfully offered to buy, and the parties entered negotiations for a ground lease that lasted several years. They exchanged several proposals, including a “counter proposal” and a “revised proposal.” Finally the both signed a document titled “Final Proposal,” a one page document. Earlier proposals stated that they were non-binding; the final did not include this language. It stated that it was “accepted by the parties subject only to approval of the terms and conditions of a formal agreement,” and Federal was to prepare a formal legal agreement. And it provided that First National could require Federal to buy the property any time over a period of ten years; and that Federal could force First National to sell at the end of ten years (the “Put and Call”). Federal never prepared a formal agreement, and decided it did not want the lease.

The court First looked at the specific language of the Final Proposal. It did not include the standard non-binding clause, and said that its terms were “hereby accepted by the parties subject to” only a formal agreement. The court then looked at the surrounding circumstances. There was the passage from counter to revised to final proposal.

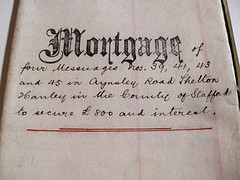

In historical terms, the California deed of trust is a recent development. Originally parties used a “mortgage” in which the property was conveyed by the buyer to the lender, subject to payment of the debt. Prior to payment of the debt, the lender was entitled to possession of the property. Use of the deed of trust with power of sale was developed to get around some of the restrictions of the mortgage and the required judicial foreclosure, a time consuming lawsuit. The property was conveyed to the buyer, who kept the right to possession, but he then conveys “nominal title” to the trustee, who, on instruction from the lender, could hold a foreclosure (by trustee’s sale) without court involvement. Borrowers and lenders concerned with the difference should contact an

In historical terms, the California deed of trust is a recent development. Originally parties used a “mortgage” in which the property was conveyed by the buyer to the lender, subject to payment of the debt. Prior to payment of the debt, the lender was entitled to possession of the property. Use of the deed of trust with power of sale was developed to get around some of the restrictions of the mortgage and the required judicial foreclosure, a time consuming lawsuit. The property was conveyed to the buyer, who kept the right to possession, but he then conveys “nominal title” to the trustee, who, on instruction from the lender, could hold a foreclosure (by trustee’s sale) without court involvement. Borrowers and lenders concerned with the difference should contact an  2923.5

2923.5 To get to the tender issue, we must first look at unconscionability. The first step taken by the court was to see if this was a “contract of adhesion.” This one was- it was a standardized contract drafted by the party with superior bargaining power without negotiation, giving the plaintiff only the choice between adhering to the contract or rejecting it. The court said yes, it could be contract of adhesion. The next step was to decide whether there were any other factors that made it unenforceable, such as if was unduly oppressive or unconscionable. Here, the plaintiff’s allegations show that it was, in two ways. First, based on the interest rates and balloon payment, and second, it was unconscionable due to his inability to replay the debt. Thus, the contract could be

To get to the tender issue, we must first look at unconscionability. The first step taken by the court was to see if this was a “contract of adhesion.” This one was- it was a standardized contract drafted by the party with superior bargaining power without negotiation, giving the plaintiff only the choice between adhering to the contract or rejecting it. The court said yes, it could be contract of adhesion. The next step was to decide whether there were any other factors that made it unenforceable, such as if was unduly oppressive or unconscionable. Here, the plaintiff’s allegations show that it was, in two ways. First, based on the interest rates and balloon payment, and second, it was unconscionable due to his inability to replay the debt. Thus, the contract could be  In seeking the injunction, the borrowers swore in declarations that at no time prior to the notice of default did the lender contact the borrower to explore options as required by

In seeking the injunction, the borrowers swore in declarations that at no time prior to the notice of default did the lender contact the borrower to explore options as required by  Connolly bought three adjacent lots in Garberville. On the northern boundary of Lot 17 they fenced off a portion so that it was part of their adjacent lot to the North. In other words, they were using a portion of the Northen end of Lot 17. They made a deal with Dobbs to sell him lot 17, with the oral agreement that Connally would keep title to the fenced off portion of 17, and there would be a “lot line adjustment” to accomplish that.

Connolly bought three adjacent lots in Garberville. On the northern boundary of Lot 17 they fenced off a portion so that it was part of their adjacent lot to the North. In other words, they were using a portion of the Northen end of Lot 17. They made a deal with Dobbs to sell him lot 17, with the oral agreement that Connally would keep title to the fenced off portion of 17, and there would be a “lot line adjustment” to accomplish that. In a recent case the lender tried to claim that, because a tenant abandoned the premises, the bad boy was triggered and the guarantor was liable.

In a recent case the lender tried to claim that, because a tenant abandoned the premises, the bad boy was triggered and the guarantor was liable.  The Rule

The Rule The listing price was $17 million. RealPro, another broker, presented a written offer to MGR for the full listing price. The listing broker then told MGR that the seller was increasing the listing price to $19,500,000. Except for the price, all other terms of the offer were acceptable. RealPro then demanded its share of the commission from MGR as a

The listing price was $17 million. RealPro, another broker, presented a written offer to MGR for the full listing price. The listing broker then told MGR that the seller was increasing the listing price to $19,500,000. Except for the price, all other terms of the offer were acceptable. RealPro then demanded its share of the commission from MGR as a Regarding checks, in 1987 the California legislature enacted

Regarding checks, in 1987 the California legislature enacted