The California Legislature enacted, and then revised, Code of Civil Procedure section 580e in response to the collapse of the housing market. As reported elsewhere, 580e now prohibits deficiencies whenever a short sale is approved by a lender on a residential property. Prior to that, it was common for lenders to claim the borrower owed the balance of the loan not paid off in the short sale. However, a decision this summer, applying the law as it existed prior to 580e, held that 580b prohibited collection of a deficiency after a short sale. The decision ignores some language in 580b, but now provides an argument for deficiency protection in short sales prior to the effective date of 580e.

****NOTE*** Since this was written, The justices of The California Supreme Court, at their weekly conference in San Francisco Wednesday Nov 22, voted 6-0 to grant review of this decision, thus it is not a final decision.

In Carol Coker v. JP Morgan Chase Bank, N.A., Coker owed $452,000 purchase money debt for her property in San Diego. She stopped paying the loan, and a notice of default was recorded. She negotiated a short sale, which Chase Bank approved subject to several conditions. The important one here is that the amount of the sale proceeds paid to Chase Bank was for the release of Chase Bank’s security interest only, and Coker was still responsible for any deficiency balance remaining on the loan after application of the proceeds received by Chase Bank. This was typical of the requirements seen by Sacramento Real Estate attorneys a few years ago; sometimes, the lender would require the seller/borrower to sign a new promissory note. The sale closed, and Chase Bank sicced a collection agency on Coker, demanding $116,686. Coker filed this lawsuit for declaratory relief, seeking a ruling from the court that 580b and 580e prohibited Chase Bank from collecting a deficiency based on this loan. 580e did not apply retroactively, so the court dismissed that claim. On appeal, however, the court found that 580b did apply to prohibit the deficiency.

In Carol Coker v. JP Morgan Chase Bank, N.A., Coker owed $452,000 purchase money debt for her property in San Diego. She stopped paying the loan, and a notice of default was recorded. She negotiated a short sale, which Chase Bank approved subject to several conditions. The important one here is that the amount of the sale proceeds paid to Chase Bank was for the release of Chase Bank’s security interest only, and Coker was still responsible for any deficiency balance remaining on the loan after application of the proceeds received by Chase Bank. This was typical of the requirements seen by Sacramento Real Estate attorneys a few years ago; sometimes, the lender would require the seller/borrower to sign a new promissory note. The sale closed, and Chase Bank sicced a collection agency on Coker, demanding $116,686. Coker filed this lawsuit for declaratory relief, seeking a ruling from the court that 580b and 580e prohibited Chase Bank from collecting a deficiency based on this loan. 580e did not apply retroactively, so the court dismissed that claim. On appeal, however, the court found that 580b did apply to prohibit the deficiency.

Some Contract defaults that may trigger acceleration

Some Contract defaults that may trigger acceleration In

In  In

In  An an

An an  In

In  The C.A.R. forms used for residential purchase agreements since the October 2002 revision have eliminated the last vestige of “passive” removal of contingencies common in the older forms. The new forms all utilize “active” written removal of contingencies, such that satisfaction of the underlying condition is not enough; there must be a written removal before a contingency is, in fact, removed. If a party does not remove it in writing, it is incumbent on the other to serve a Notice to Perform. Until all contingencies are removed in writing, Sellers always have a right to cancel. Other than the risk of cancellation, there is no penalty to the holder of the contingency if the underlying event occurs but the contingency is not removed in writing. The older C.A.R. Purchase and Sale form copyrighted 1983-1985, is different.

The C.A.R. forms used for residential purchase agreements since the October 2002 revision have eliminated the last vestige of “passive” removal of contingencies common in the older forms. The new forms all utilize “active” written removal of contingencies, such that satisfaction of the underlying condition is not enough; there must be a written removal before a contingency is, in fact, removed. If a party does not remove it in writing, it is incumbent on the other to serve a Notice to Perform. Until all contingencies are removed in writing, Sellers always have a right to cancel. Other than the risk of cancellation, there is no penalty to the holder of the contingency if the underlying event occurs but the contingency is not removed in writing. The older C.A.R. Purchase and Sale form copyrighted 1983-1985, is different.  In

In  The out of pocket rule satisfies the goal of tort claims, which is to restore the plaintiff to the financial position he was in before the fraudulent transaction, and thus awards the difference in actual value between what the plaintiff gave and what he received.

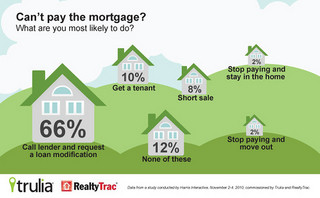

The out of pocket rule satisfies the goal of tort claims, which is to restore the plaintiff to the financial position he was in before the fraudulent transaction, and thus awards the difference in actual value between what the plaintiff gave and what he received. In Corvello v. Wells Fargo Bank, the court framed the issue: whether the bank was contractually required to offer the plaintiff a permanent loan modification after they complied with the requirements of a trial period plan (“TPP”). The answer was yes. The court first reviewed the federal programs resulting from TARP to assist homeowners. It noted that Wells Fargo, and others, signed “Servicer Participation Agreements” with the U.S. Treasury. It entitled the lenders to incentive payments for loan modifications, and requires them to follow Treasury guidelines.

In Corvello v. Wells Fargo Bank, the court framed the issue: whether the bank was contractually required to offer the plaintiff a permanent loan modification after they complied with the requirements of a trial period plan (“TPP”). The answer was yes. The court first reviewed the federal programs resulting from TARP to assist homeowners. It noted that Wells Fargo, and others, signed “Servicer Participation Agreements” with the U.S. Treasury. It entitled the lenders to incentive payments for loan modifications, and requires them to follow Treasury guidelines.